Digital Assets

一般来说,我们可以把数字资产分成几类:

- Security Tokens

- Real-World Assets

- Stablecoins

Security Tokens 证券型代币

Security Token 实际上就是 traditional security 如 stocks, bonds, funds 在区块链上的 digital representation. 通常,ST 可以代表 ownership rights (对应 stocks 股权), dividends (对应 bonds 债券), 或者其他 financial entitlements.

Benefits

- Quick Settlement

- Fractional Ownership

- Cost Reduction

- 传统的管理费可以免去. Administrative costs of traditional shareholder management

- Unlock Capital

- 企业(包括不上市的企业)都可以通过这种方式进行融资

- 24/7 Captial Market

- 比较容易理解,因为是在区块链上交易,各种检查也会在区块链上由程序(智能合约)进行,所以无需人力介入,实现全天候的交易。

- Unified Platform

- 这个很容易理解,既然都变成了 token 的形式,那么大家就都可以在同一个区块链上进行交易,避免了不同证券需要在不同平台交易的问题

Real World Asstes (RWAs)

Physical assets that are represented as digital tokens on a blockchain.

- For liquidity and access

Stable Coins

A stablecoin is a cryptocurrency that is pegged (挂钩) to another asset.

- Low volatility

- meet the requirements of sound money (健全的货币), i.e., it must be …

- Medium of Exchange

- Store of Value

- Unit of Account

- Fungible, easily divisible, and easily moved

Crypto-Collaterized 加密货币背书

- 通常 backed by other Crypto-currencies (如 ETH)

- 使用 smart contract 用于锁定其他加密货币,从而发行 stable coin. 如果抵押品的价值下跌,系统会自动触发清算

- 超额抵押 (Over-collateralization): 因为加密资产波动剧烈,系统通常要求抵押价值 > 稳定币价值(比如抵押价值要至少 150%)

- 清算 (Liquidation): 如果抵押资产价格下跌,导致抵押率低于安全阈值,智能合约会自动卖出抵押品来回购或销毁稳定币,保证稳定币仍然有足够资产支持。

Algorithmic Stable Coins

- 无抵押物

- Smart contracts adjust supply based on demand to maintain peg

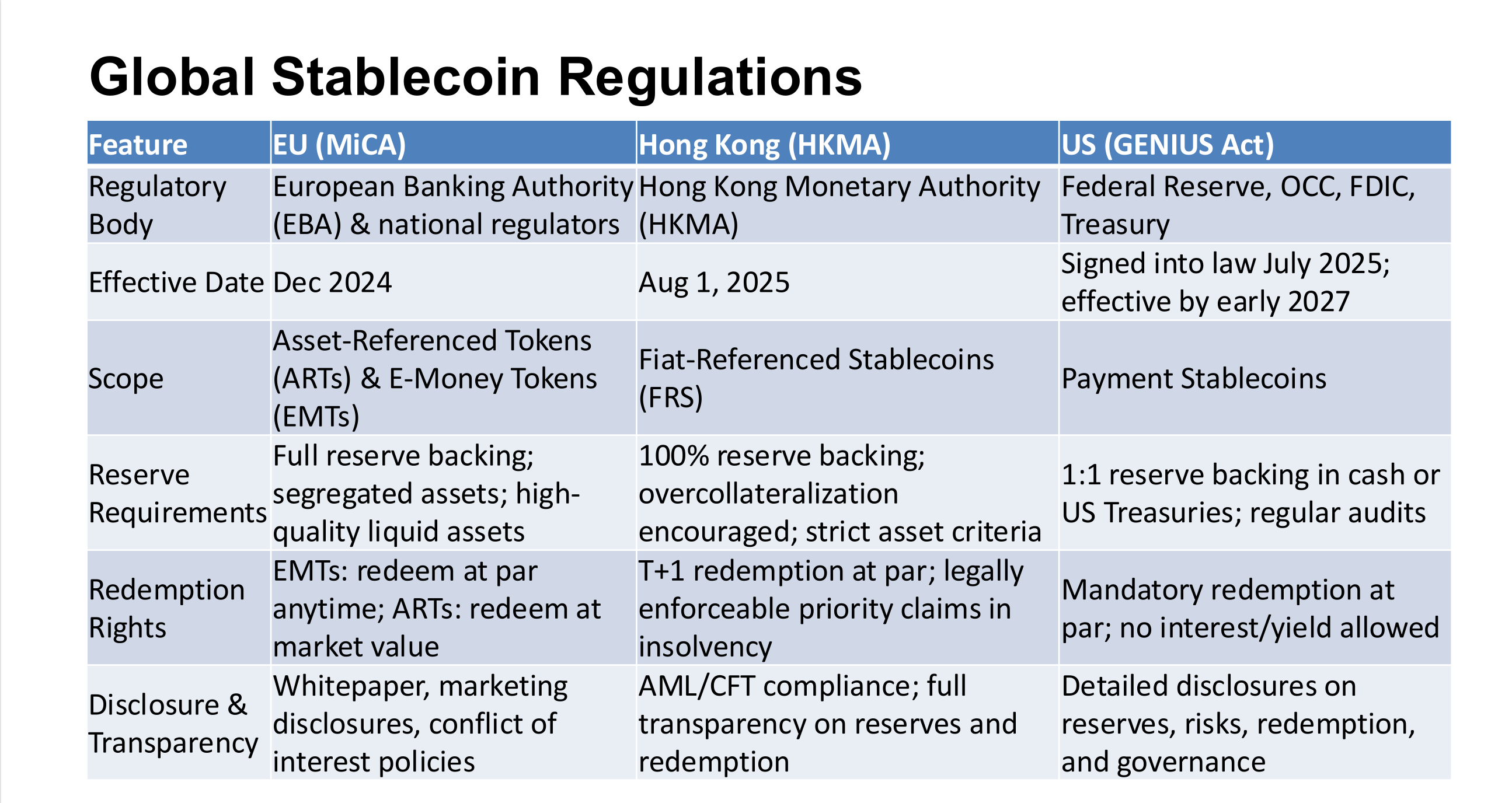

Fiat-Collaterized 法定货币背书

- Backed by real-world assets

- Controlled and owned by a central entity

- To guarantee the issuance and redeemability of the stablecoin into the underlying asset

- Regulation are required enforcing liquidity, redemption rights, and risk management standards

Stable Coin 现状

目前只有 Fiat-backed stable coins 可以流通,其余两种因为 (1) 缺乏消费者保护 (2) 脱钩风险 (3) 系统风险 等等因素还不被允许。

除了 stable coins 以外,还有一些其他选择:Bank Deposit Tokens, Central Bank Digital Currencies

Bank Deposit Tokens

- Issuer: Licensed depository institutions (banks)

- Backing: Fully backed by fiat currency deposits at the issuing bank

- Regulatory oversight: Subject to existing banking regulations

- Technology: Issued and transacted on blockchain platforms or other distributed ledger technology (DLT)

- Functionality: Programmable, enabling smart contract integration

Central Bank Digital Currencies

direct liabilities of the central bank

-

批发型 CBDC (Wholesale)

- 主要用户:商业银行、金融机构。

- 功能:用于银行间清算、证券结算、大额支付。

- 与 RTGS 的关系:

- RTGS 是现有的央行大额实时结算系统。

- 批发型 CBDC 可以作为替代方案(基于分布式账本),也可以和 RTGS 并行互补。

- 好处:提高效率,尤其是在 跨境支付和清算 场景,能缩短时间、降低成本。

-

零售型 CBDC (Retail)

- 主要用户:普通大众、企业。

- 功能:日常支付、转账、领取政府补贴。

- 使用方式:一般通过 央行或指定机构发行的数字钱包 (eWallet)。

- 意义:相当于“数字化现金”,让所有人都能直接使用央行货币。

-

批发型 → 金融机构用,替代/补充 RTGS,优化 批发市场和跨境支付。

-

零售型 → 老百姓用,替代部分纸钞和存款,强化 日常支付与普惠金融。

Decentralized Finance (DeFi)

| Defi | Traditional Finance |

|---|---|

| Smart Contracts and Decentralized,Networks | Intermediaries: Banks, Brokers,Regulators |